SUBSCRIBE TO THIS NEWSLETTER TO FOLLOW THE FEDERAL RESERVE & WALL STREET

These Charts Show How the Fed’s Secrecy Has Killed the Price Discovery Function of the Stock Market

By Pam Martens and Russ Martens: April 6, 2022 ~

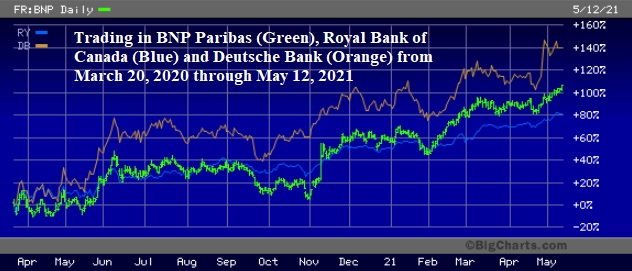

As the chart above indicates, from March 20, 2020 through May 12, 2021 the share prices of the French global bank BNP Paribas, the Canadian global bank, Royal Bank of Canada, and the German global bank, Deutsche Bank, were surging in value.

But unbeknown to the marketplace, thanks to a dark curtain the Federal Reserve of the United States drew tightly around one of its secret loan programs, the trading units of these three foreign global banks were being propped up with vast sums of cheap loans during that span of time by the Fed.

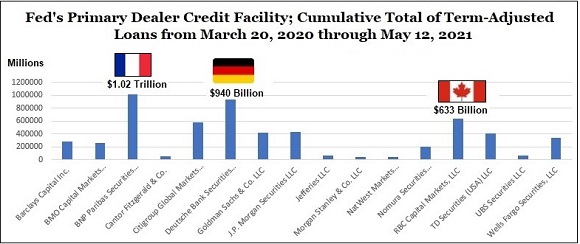

The secret loan program was the Primary Dealer Credit Facility (PDCF) – the same program the Fed used during and after the Wall Street collapse in 2008 to funnel $8.9 trillion in cumulative loans to foreign and domestic trading houses and banks, according to an audit conducted by the Government Accountability Office. The cumulative total, adjusted for the term of the loan, for PDCF loans from March 20, 2020 to May 12, 2021 was $5.78 trillion.

The Fed uses its Section 13(3) powers under the Federal Reserve Act to make these so-called emergency loans. Section 13(3) requires that the Board of Governors of the Fed has to determine by vote that there are “unusual and exigent circumstances” to launch these emergency loan programs; that the loan facility has to have “broad-based eligibility”; and the Fed has to “obtain evidence” that a participant in the facility “is unable to secure adequate credit accommodations from other banking institutions.”

The Fed only offered its PDCF loans to 24 trading houses that were mostly units of global banks. In March of 2020, when the PDCF launched, there were 5,116 banks in the United States, meaning that 24 firms out of 5,116 is not even one percent of the banks, which raises the question as to exactly how this program met the litmus test of having “broad-based eligibility.”

In effect, the Fed wasn’t attempting to help small business owners in Oshkosh; or struggling family farms in Kansas; or small towns across America whose major manufacturing plant had just shuttered operations because of the pandemic. By restricting these loans to trading houses on Wall Street, the Fed was directly targeting stock prices on Wall Street. Notably, the vast majority of stocks are owned by the richest 10 percent of households in America.

As further evidence that the Fed was directly targeting stock prices, the Fed announced it was launching the PDCF on March 17, 2020, the day after the Dow Jones Industrial Average had just plunged by 5,676 points in the prior six trading sessions. The Fed wasted no time in getting the program up and running. The first loans were made three days later on March 20.

The Section 13(3) requirement that the borrower under the emergency loan program had to show evidence that it couldn’t obtain credit from other banks would seem to be a siren call for the Fed to tread carefully. If one can’t obtain credit from other banks, it’s usually an indicator that one is not a good credit risk. But the Fed did the opposite of treading carefully. Instead of demanding the highest quality of collateral, such as Treasury securities, it accepted highly questionable collateral while still offering the loans at almost zero interest rates, that is, an interest rate of 0.25 percent.

Last Thursday, when the Fed finally released the names of the trading firms and the amounts they had borrowed from the Primary Dealer Credit Facility, it also showed the collateral they had posted for the loans. The Fed also included a set of definitions for the ambiguous categories of collateral.

For example, one peculiar collateral category was listed as “Corporate Market Instruments.” Under definitions, this was defined as: “Unsecured securities issued by private corporations, in millions of dollars.”

The PDCF was also accepting equities – yes, stocks – as collateral at a time when stocks were plunging in value. But these weren’t just any ole stocks, they were defined as “Securities representing ownership interest in a private corporation….” We can’t say for sure, but that sounds like these were not publicly-traded stocks which could be monitored minute-by-minute for price deterioration and thus the need for posting more collateral.

We emailed the media relations department at the Bank of New York Mellon, whom the Fed had assigned to value the collateral being posted under the PDCF, asking for specific examples of what was accepted under “Corporate Market Instruments” and “Equity.” We received a response from the Global Head of External Communications early yesterday afternoon, indicating that he was copying his colleague on our email, which was then followed by dead silence by the both of them for the rest of the day. (We had given a deadline of 7 p.m. last eve for a response.)

One of many examples of how this vague collateral played out is as follows: on March 24 Citigroup Global Markets borrowed $1.5 billion from the PDCF. It posted no other collateral than $1.67 billion of ambiguous “Corporate Market Instruments” to get that loan for a term of 90 days. According to the Government Accountability Office, when the Fed ran its PDCF loan facility during and after the Wall Street crash of 2008, Citigroup was the largest borrower, grabbing a cumulative total of $2.02 trillion over a span of almost two years.

The stock market’s pricing mechanism was not just thrown off in accurately pricing foreign global bank stocks because of the Fed’s secret loan programs. Two big U.S. banks’ stock pricing also seems to have been impacted by the secrecy.

As of March 29, 2020, J.P. Morgan Securities, the trading unit of the largest bank in the United States, JPMorgan Chase, had a secret outstanding loan balance of $11.85 billion at the Fed’s Primary Dealer Credit Facility. It had another secret outstanding loan balance on that date at the Fed’s repo loan facility in the amount of $37.5 billion for a combined total of $49.35 billion it needed to borrow in emergency loans from the Fed. (The Fed is only releasing bank names and borrowing amounts from its repo loan operations in 2020 and 2021 on a quarterly basis after a two-year lag, so we don’t as yet have the details on JPMorgan’s repo borrowing after March 31, 2020.)

Why was a unit of the largest bank in the United States, which was at that time reporting $1.9 trillion in deposits to the Federal Deposit Insurance Corporation, in such desperate need of liquidity from the central bank of the United States?

There was speculation on Wall Street at the time the Fed initiated its emergency repo loans in the fall of 2019 that JPMorgan Chase had played a role in triggering the lack of liquidity in the repo loan market by withdrawing large sums from its liquid reserves at the Fed. The $158 billion that JPMorgan Chase withdrew in 2019 from its liquid reserves at the Fed represented 57 percent of its total reserves at the U.S. central bank. JPMorgan Chase is a serially-charged bank. It’s inexplicable why the Fed would allow it to reduce its reserves.

We attempted to learn more about this by filing two Freedom of Information Act (FOIA) requests, one with the Federal Reserve in Washington, D.C. and one with the New York Fed, which likes to say that it follows the Federal Reserve’s FOIA guidelines, despite being a private corporation owned by the mega banks on Wall Street.

The Federal Reserve acknowledged to Wall Street On Parade on March 11, 2020 that it had 233 documents that might provide some transparency on why JPMorgan Chase was allowed to draw down $158 billion of its reserves. After taking four months to respond to what should have been a 20-business day turnaround on our Freedom of Information Act request, the Federal Reserve denied our FOIA in its entirety. (Our earlier request to the New York Fed resulted in the same kind of stonewalling. See The New York Fed Is Keeping JPMorgan’s Secrets Close to Its Chest.)

Bank of America, the second largest bank in the U.S. by assets, didn’t need to borrow at all from the Primary Dealer Credit Facility and borrowed far more modest sums from the Fed’s repo loan program than did JPMorgan Chase. But JPMorgan’s stock price performance was actually superior to that of Bank of America during the first three months of 2020 as JPMorgan was borrowing vast amounts of cheap loans from the Fed. From January 1, 2020 through March 31, 2020, JPMorgan Chase’s stock lost 35 percent while Bank of America’s decline was worse, at 40 percent.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.