American Women vs. Maga Men: The 2024 Election is a Gender Battle where Abortion Rights are the Flashpoint Chicago (Special to Informed Comment; Feature) – American women reject Trump. From his criminalizing of abortion to the ridiculing of unmarried women, from his predatory sexual harassment to racist attacks on immigrants, Trump has been very successful at repulsing female voters. Women favor Kamala Harris 58-37 in a recent NBC poll, while men prefer Trump […] |

Fundraising Appeal: Threatened Israeli (SLAPP?) Lawsuit attempts to bankrupt Informed Comment Ann Arbor (Informed Comment) – Running a small independent publication on controversial issues is fraught with problems. One of them is that people threaten to sue you. It happens time to time. For some reason the Israelis are particularly trigger-happy about threatening lawsuits. Many years ago the notorious MEMRI campaign to translate only the worst […] |

Protesting Cornell University’s Suspension and threatened Deportation of graduate Student Momodou Taal for Protest Committee on Academic Freedom | Middle East Studies Association | – Dear Interim President Kotlikoff, Provost Bala, Dr. Lombardi and Ms. Liang: We write on behalf of the Middle East Studies Association of North America (MESA) and its Committee on Academic Freedom to express our extreme concern about your decision to temporarily suspend Cornell graduate […] |

Hezbollah is not Finished Yet ( The National ) – The assassination of Hezbollah secretary general Hassan Nasrallah in Beirut will not diminish the group he once led. The killing demonstrates the counterintuitive notion that eliminating the head of an organisation does not always destroy it. Hezbollah has a bureaucratic set-up, with a robust ideology and communal support. Any armed […] ( The National ) – The assassination of Hezbollah secretary general Hassan Nasrallah in Beirut will not diminish the group he once led. The killing demonstrates the counterintuitive notion that eliminating the head of an organisation does not always destroy it. Hezbollah has a bureaucratic set-up, with a robust ideology and communal support. Any armed organisation that benefits from all three tends to survive the death of its leader. The October 7 attacks led by Hamas proved to be a conundrum for Hezbollah. Before that, the group had been challenged by Lebanese protesters, including by members of the Shiite community, since 2019, for controlling a corrupt Parliament and allowing Iran to violate Lebanon’s sovereignty. The war in Gaza allowed Hezbollah to deflect attention from its domestic woes, by launching rockets against Israel, in solidarity with Hamas, but not doing enough to risk immediate Israeli retaliation. It forced Israel to keep some military forces in the north and the evacuation of civilians from there. Nasrallah’s death will most likely lead to a significant proportion of the Lebanese public rallying behind Hezbollah. The protests in 2019 were a domestic matter. With the assassination having been carried out by a foreign state, Israeli Prime Minister Benjamin Netanyahu may end up uniting the Lebanese people in a way that has been elusive since the end of the nation’s civil war in 1991. In 1992, the year after the civil war ended, Israeli helicopters killed Hezbollah’s then secretary general, Abbas Al Musawi, as well as his wife and six-year-old son in a motorcade. In Ronen Bergman’s book, Rise and Kill First: The Secret History of Israel’s Targeted Assassinations, he documents how some Israeli military figures had opposed the killing as “Hezbollah was not a one-man show, and [Al] Musawi was not the most extreme man in its leadership”. Indeed, they warned, he “would be replaced, perhaps by someone more radical”. Al Musawi was succeeded by Nasrallah, who proved to be more charismatic and eloquent. At the time, Hezbollah was a small militia, employing suicide bombs as its most powerful weapon. When Nasrallah emerged, he put a military commander, Fouad Shukr, who was killed in July in a similar strike, in charge of stepping up sophisticated guerrilla attacks on Israeli forces in the south of Lebanon. These attacks, as well as rocket launches, compelled them to withdraw in 2000, marking a rare and significant Israeli loss to an Arab military force. In this respect, history is a study of irony, of unintended consequences, as Israel’s assassination scored a vendetta, only to witness a replacement who proved to be a more adept leader – a possibility that exists with Nasrallah’s successor. The group has a top-down, military-style bureaucracy, while at the same time maintaining a diffuse and decentralised military command structure to operate if higher-level commanders are killed during battle. Its bureaucracy, with clear chains of command, will enable it to select a new leader. It has routinised its leadership succession, whereby the secretary general is appointed by a council, so that the legitimacy of the successor derives from the position and not the individual. As a tactic, Israeli assassinations do not address the underlying problems of conflict in the region. Strategically they backfire, as assassinations might lead to unpredictable outcomes, like in 1992 Hezbollah adheres to the “Axis of Resistance” ideology, along with Iran, the Houthis of Yemen and Hamas in Palestine, based on resistance to Israel and the US. However, the group also blends Lebanese nationalism, as well as a southern Lebanese identity, invoking how the region has suffered from Israeli actions since its first invasion in 1978. The ideology does not depend on a leader for its articulation or propagation. As a set of ideas, it existed before Nasrallah became the leader in 1992. Hezbollah earned credit for driving Israeli troops out of Lebanon as 2000. One of the factors behind this success was the willingness of the group’s members and followers to sacrifice their lives for their cause. Their propaganda focuses on seeking inspiration from the success of Iran’s revolution in 1979. This dynamic contributes to the third factor Hezbollah enjoyed: popular support within certain communities. The group’s presence in the south of Lebanon is enabled by a network of sympathetic Arab villages, that goes beyond just its Shiite Muslim base, including some members of the Christian community. There is an argument to be made that, instead of waging war against Hezbollah, Israel could have declared a ceasefire in Gaza as the one-year anniversary of the conflict approaches. This would have done far more damage to Hezbollah by depriving it of the rhetorical oxygen it has often used to justify its rocket attacks, which the group said it would have ceased once the fighting in Gaza ended. As a tactic, Israeli assassinations do not address the underlying problems of conflict in the region. Strategically they backfire, as assassinations might lead to unpredictable outcomes, like in 1992. In the long term, Israel’s tactical military strikes are no panacea for political violence compared to multilateral peace and development strategies. Both the US and France, permanent members of the UN Security Council, had pushed for implementing the 2006 Security Council Resolution 1701, which calls for the Lebanese army and UN peacekeepers to monitor the area south of Lebanon on the border with Israel, creating a buffer zone. A cessation of hostilities in Gaza and Lebanon would have been the best long-term solution, achieving a more sustainable security than continued conflict that only creates a new generation of Lebanese and Palestinians seeking atonement from Israel. As the one-year anniversary of the war in Gaza is upon us, it appears that Mr Netanyahu is seeking another year of conflict to maintain his hold on power. Reprinted from The National with the author’s permission. —– Bonus video added by Informed Comment: Al Jazeera English: “Hezbollah ‘prepared’ for Israel’s ground incursion: Hezbollah deputy chief” |

Old posts you may have missed

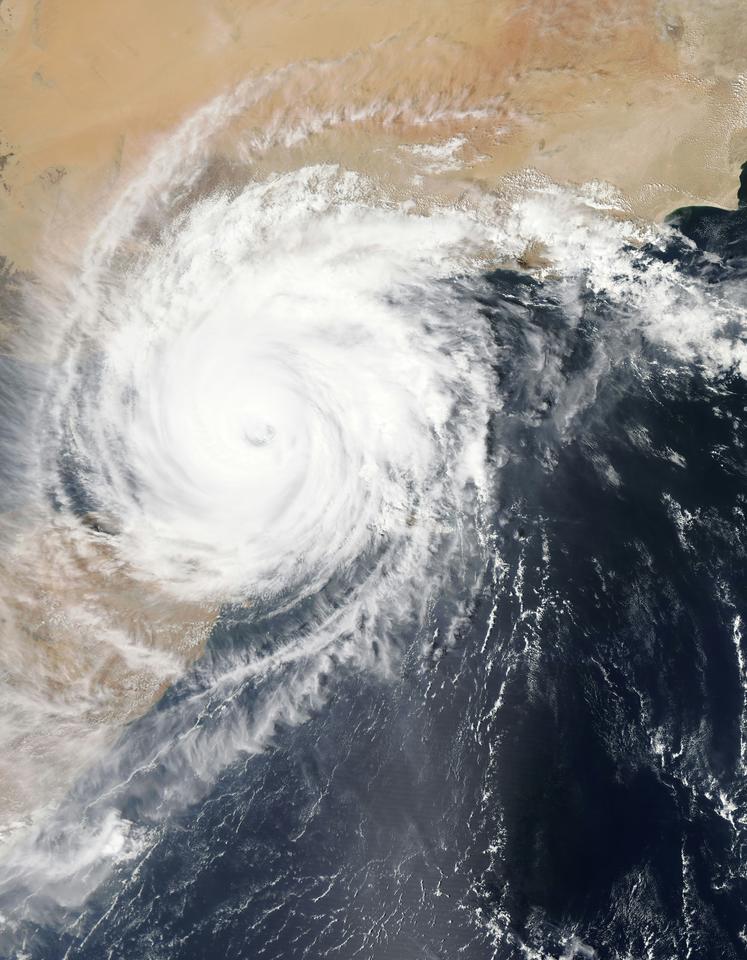

Why an Israeli invasion of Lebanon is a Mistake The Battle for the Soul of American Science: The Pentagon goes to School The Path to Nasrallah’s Assassination Climate Change-Driven Hurricanes and Wildfires are causing Home Insurance Rates to Skyrocket Water as a Weapon of War in Gaza (The New Lines Institute) Climate Change-Driven Hurricanes and Wildfires are causing Home Insurance Rates to Skyrocket Climate Change-Driven Hurricanes and Wildfires are causing Home Insurance Rates to SkyrocketBy Andrew J. Hoffman, University of Michigan | – (The Conversation) – Millions of Americans have been watching with growing alarm as their homeowners insurance premiums rise and their coverage shrinks. Nationwide, premiums rose 34% between 2017 and 2023, and they continued to rise in 2024 across much of the country. To add insult to injury, those rates go even higher if you make a claim – as much as 25% if you claim a total loss of your home. Why is this happening? There are a few reasons, but a common thread: Climate change is fueling more severe weather, and insurers are responding to rising damage claims. The losses are exacerbated by more frequent extreme weather disasters striking densely populated areas, rising construction costs and homeowners experiencing damage that was once more rare. Parts of the U.S. have been seeing larger and more damaging hail, higher storm surges, massive and widespread wildfires, and heat waves that kink metal and buckle asphalt. In Houston, what used to be a 100-year disaster, such as Hurricane Harvey in 2017, is now a 1-in-23-years event, estimates by risk assessors at First Street Foundation suggest. In addition, more people are moving into coastal and wildland areas at risk from storms and wildfires. Just a decade ago, few insurance companies had a comprehensive strategy for addressing climate risk as a core business issue. Today, insurance companies have no choice but to factor climate change into their policy models. Rising damage costs, higher premiumsThere’s a saying that to get someone to pay attention to climate change, put a price on it. Rising insurance costs are doing just that. Increasing global temperatures lead to more extreme weather, and that means insurance companies have had to make higher payouts. In turn, they have been raising their prices and changing their coverage in order to remain solvent. That raises the costs for homeowners and for everyone else. The importance of insurance to the economy cannot be understated. You generally cannot get a mortgage or even drive a car, build an office building or enter into contracts without insurance to protect against the inherent risks. Because insurance is so tightly woven into economies, state agencies review insurance companies’ proposals to increase premiums or reduce coverage. The insurance companies are not making political statements with the increases. They are looking at the numbers, calculating risk and pricing it accordingly. And the numbers are concerning. The arithmetic of climate riskInsurance companies use data from past disasters and complex models to calculate expected future payouts. Then they price their policies to cover those expected costs. In doing so, they have to balance three concerns: keeping rates low enough to remain competitive, setting rates high enough to cover payouts and not running afoul of insurance regulators. But climate change is disrupting those risk models. As global temperatures rise, driven by greenhouse gases from fossil fuel use and other human activities, past is no longer prologue: What happened over the past 10 to 20 years is less predictive of what will happen in the next 10 to 20 years. The number of billion-dollar disasters in the U.S. each year offers a clear example. The average rose from 3.3 per year in the 1980s to 18.3 per year in the 10-year period ending in 2024, with all years adjusted for inflation. With that more than fivefold increase in billion-dollar disasters came rising insurance costs in the Southeast because of hurricanes and extreme rainfall, in the West because of wildfires, and in the Midwest because of wind, hail and flood damage. Hurricanes tend to be the most damaging single events. They caused more than US$692 billion in property damage in the U.S. between 2014 and 2023. But severe hail and windstorms, including tornadoes, are also costly; together, those on the billion-dollar disaster list did more than $246 billion in property damage over the same period. As insurance companies adjust to the uncertainty, they may run a loss in one segment, such as homeowners insurance, but recoup their losses in other segments, such as auto or commercial insurance. But that cannot be sustained over the long term, and companies can be caught by unexpected events. California’s unprecedented wildfires in 2017 and 2018 wiped out nearly 25 years’ worth of profits for insurance companies in that state. To balance their risk, insurance companies often turn to reinsurance companies; in effect, insurance companies that insure insurance companies. But reinsurers have also been raising their prices to cover their costs. Property reinsurance alone increased by 35% in 2023. Insurers are passing those costs to their policyholders. What this means for your homeowners policyNot only are homeowners insurance premiums going up, coverage is shrinking. In some cases, insurers are reducing or dropping coverage for items such as metal trim, doors and roof repair, increasing deductibles for risks such as hail and fire damage, or refusing to pay full replacement costs for things such as older roofs. Some insurances companies are simply withdrawing from markets altogether, canceling existing policies or refusing to write new ones when risks become too uncertain or regulators do not approve their rate increases to cover costs. In recent years, State Farm and Allstate pulled back from California’s homeowner market, and Farmers, Progressive and AAA pulled back from the Florida market, which is seeing some of the highest insurance rates in the country. State-run “insurers of last resort,” which can provide coverage for people who can’t get coverage from private companies, are struggling too. Taxpayers in states such as California and Florida have been forced to bail out their state insurers. And the National Flood Insurance Program has raised its premiums, leading 10 states to sue to stop them. About 7.4% of U.S. homeowners have given up on insurance altogether, leaving an estimated $1.6 trillion in property value at risk, including in high-risk states such as Florida. No, insurance costs aren’t done risingAccording to NOAA data, 2023 was the hottest year on record “by far.” And 2024 could be even hotter. This general warming trend and the rise in extreme weather is expected to continue until greenhouse gas concentrations in the atmosphere are abated. In the face of such worrying analyses, U.S. homeowners insurance will continue to get more expensive and cover less. And yet, Jacques de Vaucleroy, chairman of the board of reinsurance giant Swiss Re, believes U.S. insurance is still priced too low to fully cover the risk from climate change. Climate change is a major factor in the rising cost of insurance. Join us for a special free webinar with experts Andrew Hoffman of the University of Michigan and Melanie Gall of Arizona State University to discuss the arithmetic behind these rising rates, what climate change has to do with it, and what may be coming in your future insurance bills. Wednesday, October 9, 2024, 11:30 a.m. PT/2:30 p.m. ET. Andrew J. Hoffman, Professor of Management & Organizations, Environment & Sustainability, and Sustainable Enterprise, University of Michigan This article is republished from The Conversation under a Creative Commons license. Read the original article. |

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.