SUBSCRIBE TO THIS NEWSLETTER TO RECEIVE IT IN A TIMELY MANNER

At Year End, 4,127 U.S. Banks Held $7.7 Trillion in Uninsured Deposits; JPMorgan Chase, BofA, Wells Fargo and Citi Accounted for 43 Percent of That

By Pam Martens and Russ Martens: May 11, 2023 ~

If the dark secrets about the U.S. banking system that federal regulators have been keeping since the financial crash of 2008 are allowed to be aired in public Congressional hearings as a result of the current banking crisis – and mainstream media will grow a backbone and cover those hearings – it could help the U.S. avoid a catastrophic financial reckoning down the road.

For years, Wall Street On Parade has been reporting that just four banks in the U.S. control more than 85 percent of all the opaque derivatives in the banking system. We have also regularly reported how federal agencies have singled out these four banks for posing systemic risk to the financial stability of the United States. We’re talking about JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank.

On March 30, we crunched the numbers from the regulatory filings made by these banks (call reports) and reported that as of December 31, 2022, these four banks held a combined $3.286 trillion in uninsured domestic deposits. (Federal deposit insurance is capped at $250,000 per depositor per bank. Uninsured deposits taking flight were a key element in the recent bank runs that led to the second, third and fourth largest bank failures in U.S. history.) As of December 31, 2022, JPMorgan Chase Bank N.A. held $2.015 trillion in deposits in domestic offices, of which $1.058 trillion were uninsured; Bank of America held $1.9 trillion in deposits in domestic offices, of which $909.26 billion were uninsured; Wells Fargo held $1.4 trillion in deposits in domestic offices, of which $721.1 billion were uninsured; and Citibank N.A. (parent, Citigroup) held $777 billion in deposits in domestic offices, of which $598.2 billion were uninsured.

We can now put that $3.286 trillion figure into sharper perspective. On May 1, the FDIC released its report on “Options for Deposit Insurance Reform.” Without mentioning that just four banks controlled $3.286 trillion of uninsured deposits at year end, the FDIC report did provide the figure of $7.7 trillion as the total of uninsured domestic deposits held by all banks at the end of 2022.

That means that just these four banks held 43 percent of all uninsured deposits at 4,127 federally insured commercial banks in the U.S. as of year end 2022.

The FDIC report reads as follows:

“Following the 2008-2013 banking crisis, the reliance by the U.S. banking system on uninsured deposits grew dramatically, both in dollar volume and as a proportion of overall deposit funding. From year-end 2009 through year-end 2022, uninsured domestic deposits at FDIC-institutions increased at an annualized rate of 9.8 percent, from $2.3 trillion to $7.7 trillion.”

Give your brain a few moments to thoroughly digest that statement. Federal regulators have known since the 1930s that uninsured deposits are the most likely to bolt in a banking crisis, and yet, after the worst banking crisis in 2008 since the Great Depression, both Congress and federal regulators have allowed uninsured deposits to more than triple at U.S. banks – as well as to become concentrated at just four banks.

If ever there was a screaming call to dramatically restructure federal oversight of banks – this is it.

The average American has no idea of just how dangerously concentrated banking has become in the United States. That’s because mainstream media never puts this information on the front pages of newspapers or reports it on the evening TV news.

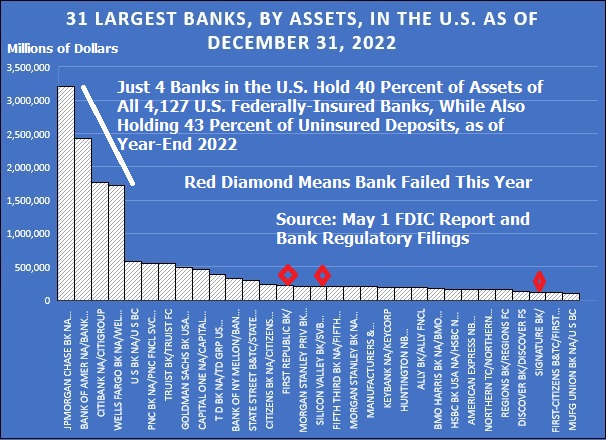

We decided to help fill in this void by creating the graphic above, using data from regulatory filings. Our graphic shows the consolidated assets of the 31 largest banks in the U.S., which total $16.012 trillion.

The same four banks discussed above, JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank, represent 0.0969 percent of the total 4,127 federally-insured commercial banks in the U.S. – and yet they are allowed by federal regulators and Congress to control a mind-boggling $9 trillion in consolidated assets.

All 4,127 federally-insured commercial banks in the U.S. held $22.3 trillion in assets as of December 31, 2022 according to the Federal Deposit Insurance Corporation’s Statistics at a Glance. The $9 trillion in assets held by just these four banks represents 40 percent of the total assets of all 4,127 banks.

Also disturbing, the 31 banks on the graph above held $16.012 trillion in assets, or 72 percent of the total assets of all 4,127 banks in the U.S. Three of those banks have failed this year.

How did this happen? See our article: In 16 Years, the Fed Has Approved 4,506 Bank Mergers and Denied One.

Against this backdrop, it is nothing short of gross incompetence (and/or regulatory capture) that federal regulators allowed JPMorgan Chase, already the largest bank by assets, deposits, derivatives and riskiness, to purchase the failed bank, First Republic, on May 1.

LINK

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.